The SaaSpocalypse Paradox: Why Growing Software is Crashing

How AI agents turned the world's most predictable business model into a melting ice cube.

Everything is moving so fast in tech right now that my thinking on this piece changed three times before I could even hit publish. I work in software, I build apps, and frankly, it’s boggling my mind.

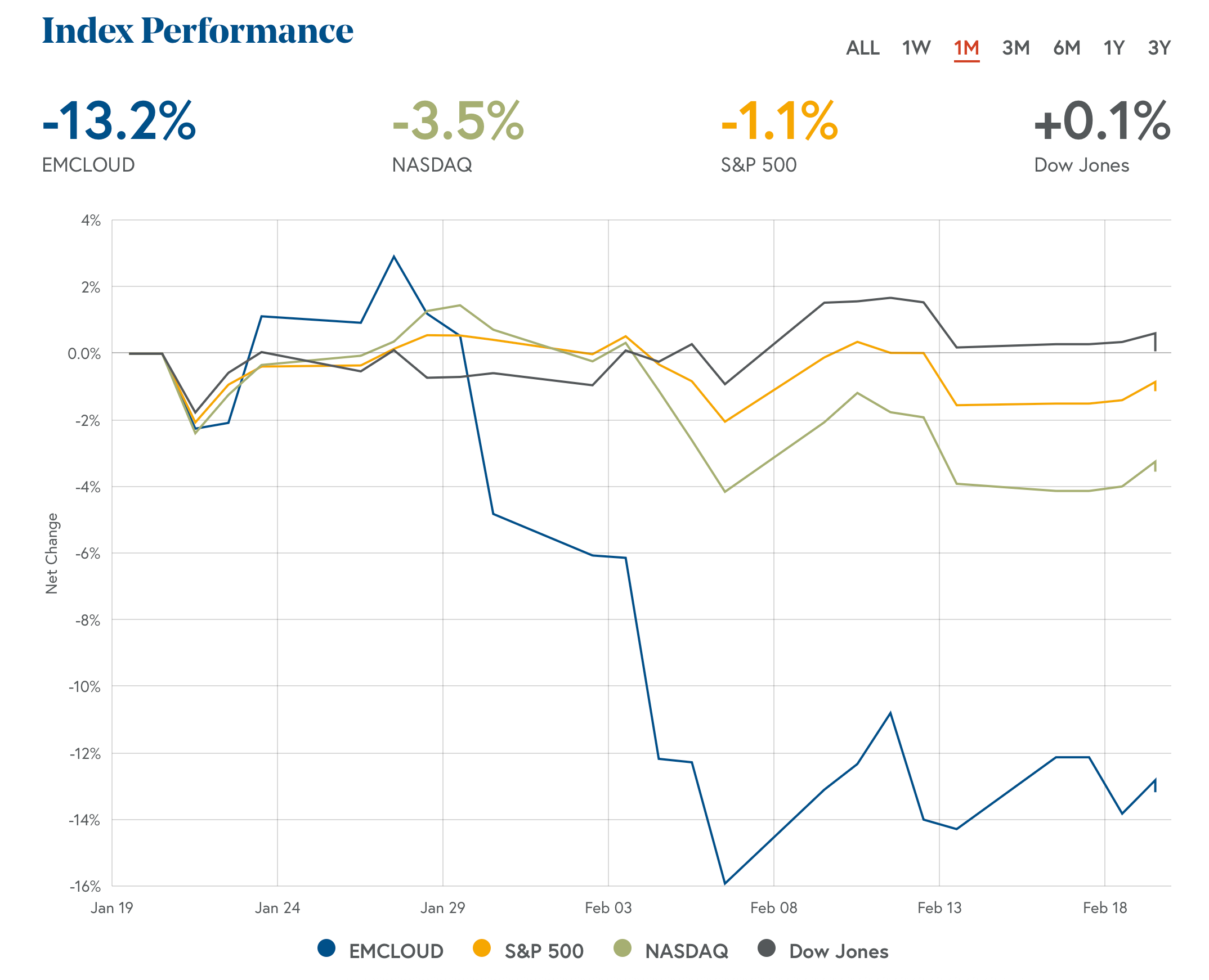

On January 30th, Anthropic launched Claude Cowork. Within 48 hours, $285 billion in market cap evaporated from global software stocks. Traders started calling it the “SaaSpocalypse.” The weird part? The companies being sold off weren’t failing.

Atlassian just reported $1.6B in revenue, 23% growth, and record enterprise deals. The stock dropped anyway. Monday.com posted 27% growth and saw their stock crater 21% in a single day.

Wall Street wasn’t grading the quarter; it was grading the model. And the model has a problem that record revenue can’t fix.

I don’t claim to be an expert. I’m just a guy who loves business, loves building, and is trying to make sense of the noise. Anyone claiming to have a “lock” on the future of software right now is mighty full of themselves. But I’ve been living inside this industry long enough to have a few strong opinions on how the next few years play out.

Here’s where I’ve landed.

Small SaaS is Dead

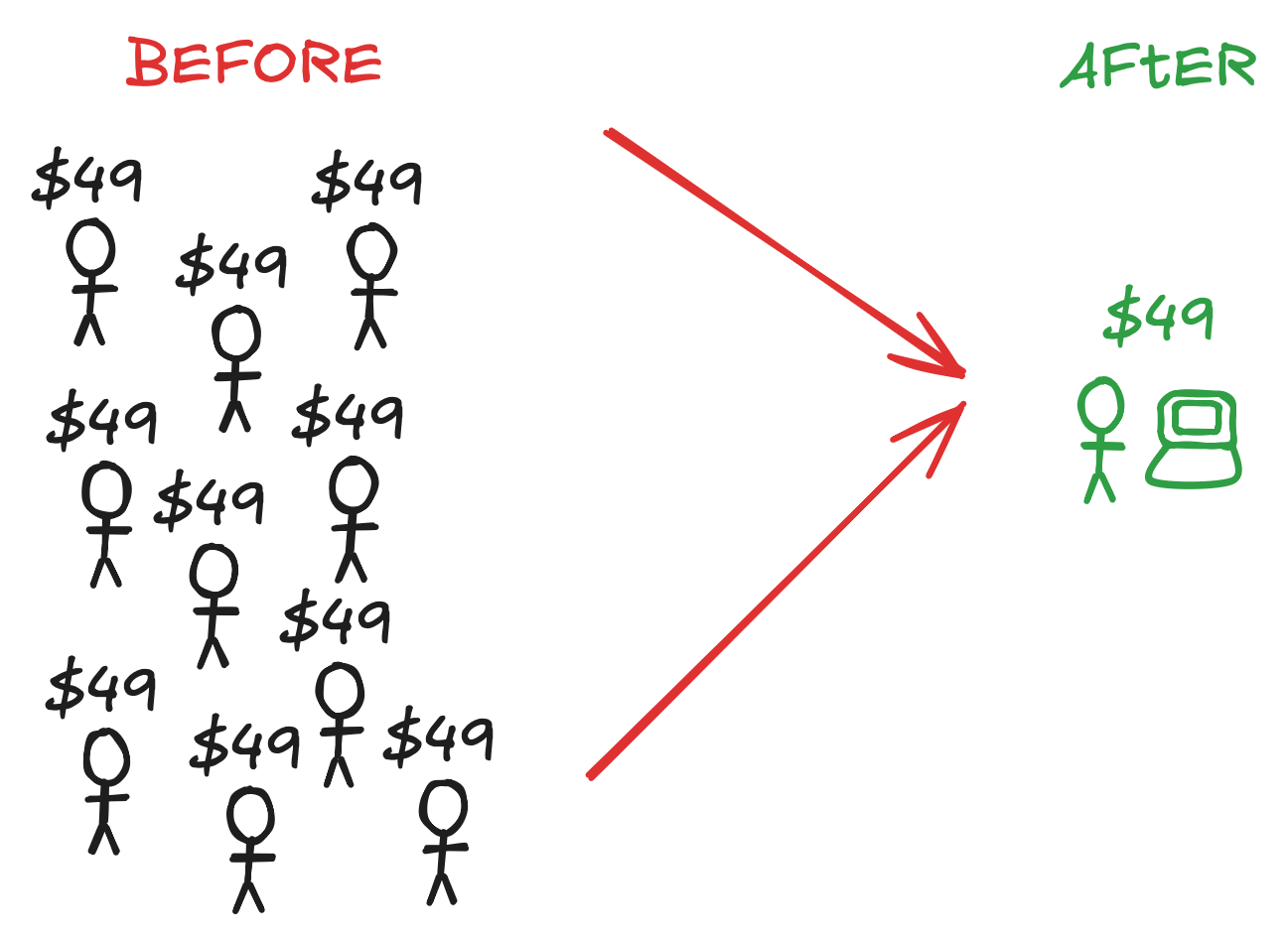

This I think is a given. The $10-49/month offerings, the really cheap tools that had a singular purpose, they’ll just be built internally.

Calendly is the easy one to pick on. In 2021, we were happy to pay $15 a month to Calendly just to avoid an email thread. It was a fair trade. But in 2026, when a junior dev can spin up a custom scheduling agent in an afternoon using Claude, that $15 starts to feel like a tax. We’re seeing the same thing happen to Jasper in content and Baremetrics in analytics. These aren’t bad companies; they’re just ‘feature-SaaS’ in a world where features have become free.

These small SaaS providers must either become larger, or have something that’s so difficult to maintain the $49/mo fee is a must pay.

Big SaaS Needs an Unbundling

On the opposite end there’s the big SaaS. The ones that are currently getting pummeled on Wall Street. They’re struggling because it’s too heavy to move. They’re struggling because they charge for more than the end user really wants and needs.

For over twenty years, the giants like Salesforce and Atlassian were the ultimate “safe bets” because they owned the seat. If you hired 1,000 people, you bought 1,000 seats. It was a predictable, linear money machine. But, in the 2026 “SaaSpocalypse” that seat count has turned from a growth engine into a massive liability.

This is why the Q4 earnings cycle has been surreal for these giants. The headlines show revenue growth, the highlights show they’re closing massive deals. The footnotes are starting to tell a different story though: seat counts are shrinking while usage is skyrocketing.

The math behind it is simple. If an AI agent can handle the workload of ten humans within a tool then the company doesn’t need ten Salesforce seats anymore; they need one “agent license.” In the current per-seat model, that’s a 90% revenue haircut for the software vendor.

To survive the shift, these big names (Salesforce, Atlassian, SAP, Workday) have to find a way to unbundle the “seat” from “value.” If they don’t, it could be a slow ride to irrelevancy as enterprises migrate elsewhere.

Salesforce is already dabbling; they even have an Agentic Enterprise License Agreement (AELA) available which starts the pivot away from number of people logged in to charging for actual value.

The transition will be messy. It’s hard to define “value” and “outcome” for a project management tool, and even harder to convince a customer to pay for a “shipped feature” instead of a monthly subscription.

These giants are essentially trying to rebuild their engines while flying the plane. Some will pull it off, others will have a crash landing.

Commoditization all the way down

The third possible outcome I see is commoditization. A world where code isn’t the bottleneck means that I can very easily spin up a CRM that competes with Salesforce, or a project tracking tool to compete with Jira.

Will this tool be as feature-rich? No. But it can be highly specific. A CRM for something super niche could take a bite out of Salesforce and the new AI tooling allows for more than one bite.

There could be hundreds of CRMs within a few months, all with a handful of employees able to compete against the behemoth Salesforce.

SaaS companies used to compete on who had the best UI, the cleanest dashboards, and the prettiest buttons. In the future, all of this can happen in minutes with a prompt on the weekend.

Even worse for some of the established names it could happen without UIs at all. Future iterations of the CRM or project tracker might just skip the UI entirely and go the agent route. When an agent can pull data, cache it, act on it without ever logging in, the “premium” feel of a $200/month platform starts to look a lot like a lick of expensive paint on a commodity wall.

The DIY Approach to All

Finally, the most radical take is that companies just build it themselves. Want a CRM? Build it internally. Want a project tracker? Build that too. This, of course, would require an internal team to build and maintain and that “maintain” could be expensive, which is why this is a slim chance in my eyes.

We have already seen the first shot across the bow though with this approach from Klarna. They famously announced they were shutting down Salesforce and Workday to “build their own” with AI. The reality of it ended up a bit messier. They actually migrated many functions to smaller, more nimble SaaS tools like Deel, but the intent was a signal to the entire market.

“Build vs Buy” has always been a landslide victory for “Buy.” That landscape is changing. AI collapses initial buildout costs from $500k down to $20k or less. The only thing stopping a DIY revolution now is the maintenance trap.

That first version is easy, but the years of edge-case handling, security patches, and API updates are still a grind. Companies that stick with SaaS won’t do it because they can’t build the code; they’ll do it because they don’t want to own the maintenance.

The Odd Paradox

So those are the four paths I think we could take:

No more small tool SaaS

Big SaaS has to figure out a different path

Commoditization could destroy margins

A DIY approach could further disrupt the market

It’s always interesting to find the one bit of data that contradicts everything you just wrote.

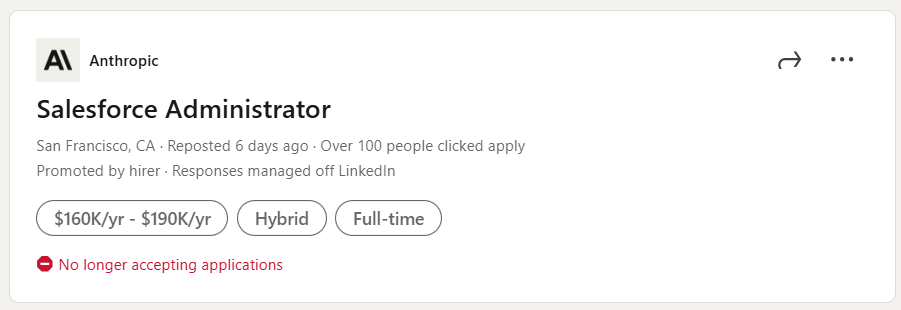

Anthropic, the very company that released the “seat-killing” Claude Cowork, spent the early weeks of 2026 hiring a Salesforce Administrator.

Huh. It’s the perfect symbol for where we are. The people building the future aren’t quite ready to live in it yet. Even the leaders of the AI revolution still need the “System of Record” to keep the lights on and the revenue flowing.

While this doesn’t mean the old model is safe, it shows that the giants have a “grace period.” The “SaaSpocalypse” isn’t a single day of destruction; it’s a long, messy re-pricing of the entire software world.

What Will Last?

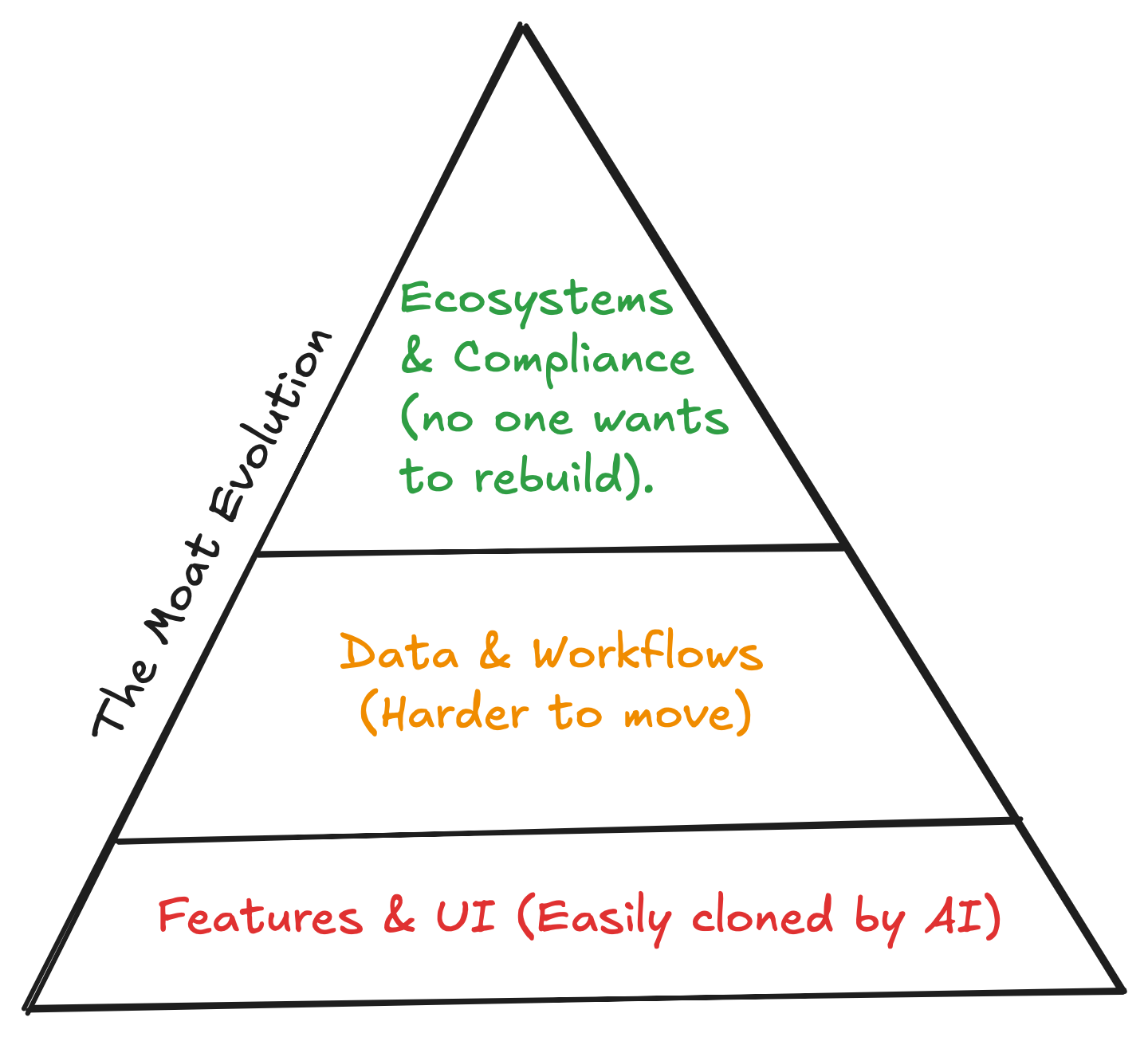

If the code is a commodity and the seats are melting, only three things really matter:

Irreplaceable Ecosystems: You can clone Jira’s task list in a weekend, but you can’t clone ten years of enterprise security audits and 5,000 third-party integrations. The “plumbing” is a much better moat than the “paint.”

The “Must-Be-Right” Layer: AI is great at “guessing” (marketing copy, basic CRM notes), but it’s still dangerous for things that require 100% accuracy. Software that handles payroll, taxes, and legal compliance, the “deterministic” stuff, will be the last to fall.

The Outcome Pioneers: The winners will be the companies that stop selling “tools for humans” and start selling “results for businesses”. If you can prove your software closes the deal, you can charge for the win, not the login.

Overall, I don’t think the market is wrong. The likes of Atlassian, Salesforce, and Workday have to go through painful changes to survive this shift. But they have the data, they have the ecosystems, and for now, they still have the administrators.

SaaS isn’t dead. But the “original bargain,” the idea that we’ll pay a monthly tax to avoid the friction of building our own tools, is gone. The friction just got a whole lot cheaper to remove and that cost is dropping by the day.

Grab your popcorn.