The Great Implementation: Turning Citrini’s 2028 Crisis into a Payout

How to position your portfolio and your career for an economy that works for agents, not humans.

It took me a while to get through. Hey, it’s a behemoth, give me a break. But I did just finish reading Citrini’s post, “THE 2028 GLOBAL INTELLIGENCE CRISIS.”

I’ve seen rebuttals and I’ve seen the counterarguments, but I’ve not yet seen anyone say, “Okay, let’s assume this is the path, what next?” So, I sat down with a pen and paper and began noodling a bit. Below are my thoughts on two topics:

What you can do as a public market investor

What you can do as a W-2 employee, or even just a person who needs to work to earn a living

I’ll lead with the same disclaimer as Citrini:

This isn’t bear porn or AI doomer fan-fiction. The sole intent of this piece is modeling a scenario that’s been relatively underexplored.

My thoughts below assume the fiction proposed by Citrini turns out to be correct.

The tl;dr on Citrini

As mentioned, that’s a massive article. In an effort to save you from reading the whole thing, here’s an AI-generated tl;dr:

The “Great Implementation Cycle” (GIC) argues that we are moving from the “build” phase of AI to the “use” phase, where the real economic value shifts from the companies selling chips to the businesses that successfully integrate AI to cut costs. This transition will likely trigger a massive productivity boom that keeps inflation low while allowing interest rates to stay higher for longer, favoring “old economy” companies that can automate their operations. For the individual, this means the highest rewards will go to “operators” who can bridge the gap between complex AI capabilities and real-world business results.

AI used for good! But, of course, that’s the premise of the article. We use it for good. Humans that previously did the “good” lose out. Humans losing out equals less money flow. Less money flow means more humans end up losing out. Rinse and repeat.

Public Market Investing

Investing for the last two decades has been pretty easy... especially if you’ve been investing in tech. It would seem those easy days are behind us if Citrini’s piece is the law of the land.

The Bad

The article called out DoorDash, Visa, Mastercard, and “long-tail SaaS” as potential victims of the shift, and yeah, I can see them having some difficulties in the future.

I’d bucket the “high risk” category into a few items:

Workflow & task management

Intermediaries

Administrative tooling

Human-centric service platforms

Workflow & task management covers companies mentioned in the article like Asana, Monday.com, and Atlassian (Jira / Confluence). If following the “2028 GIC” logic, these companies are the first to be disrupted because businesses will easily build their own internal “organizers” for free.

These types of tools rely heavily on per-seat pricing, and I already shared in a prior post why I think this is ripe for disruption anyway, so I can’t say I disagree here. There has to be a fundamental shift in their go-to-market strategy to be successful.

Intermediaries like Visa, Mastercard, and Amex will be disrupted, the article claims, because they’re essentially friction monetizers. Agentic workflows aren’t humans. Humans reach for the easy and familiar; agents could go through a bit of pain to optimize, and the rationale here is that they *will* optimize.

NOTE: I have to make sure to call out the fees misconception here... Visa and Mastercard charge about 0.15% of a transaction. That 2.5% - 3% you frequently seen thrown around is everyone else taking a cut. You’re not going to disrupt 0.15% too easily.

There’s been decades of attempted disruption here, and these are already massive companies. While I don’t think it’ll be an overnight “win” for stablecoins, I do think disruption will come, albeit from companies like Square, Shopify, or Toast that could build large enough network effects to create a closed-loop payment system with on-ramps/off-ramps and benefits for keeping money on-network (I should write this post next :) ).

Administrative tools are things like DocuSign and Intuit. If an AI agent can suddenly navigate the tax code or execute a legal agreement, then perhaps there’s not much need for these tools. This one I struggle with a bit. There will be some winners here and many losers. I won’t dive into individuals, but a fantastic recent read on “Why does DocuSign have 7,000 employees” really hits on why this might not be as easy to disrupt as it appears.

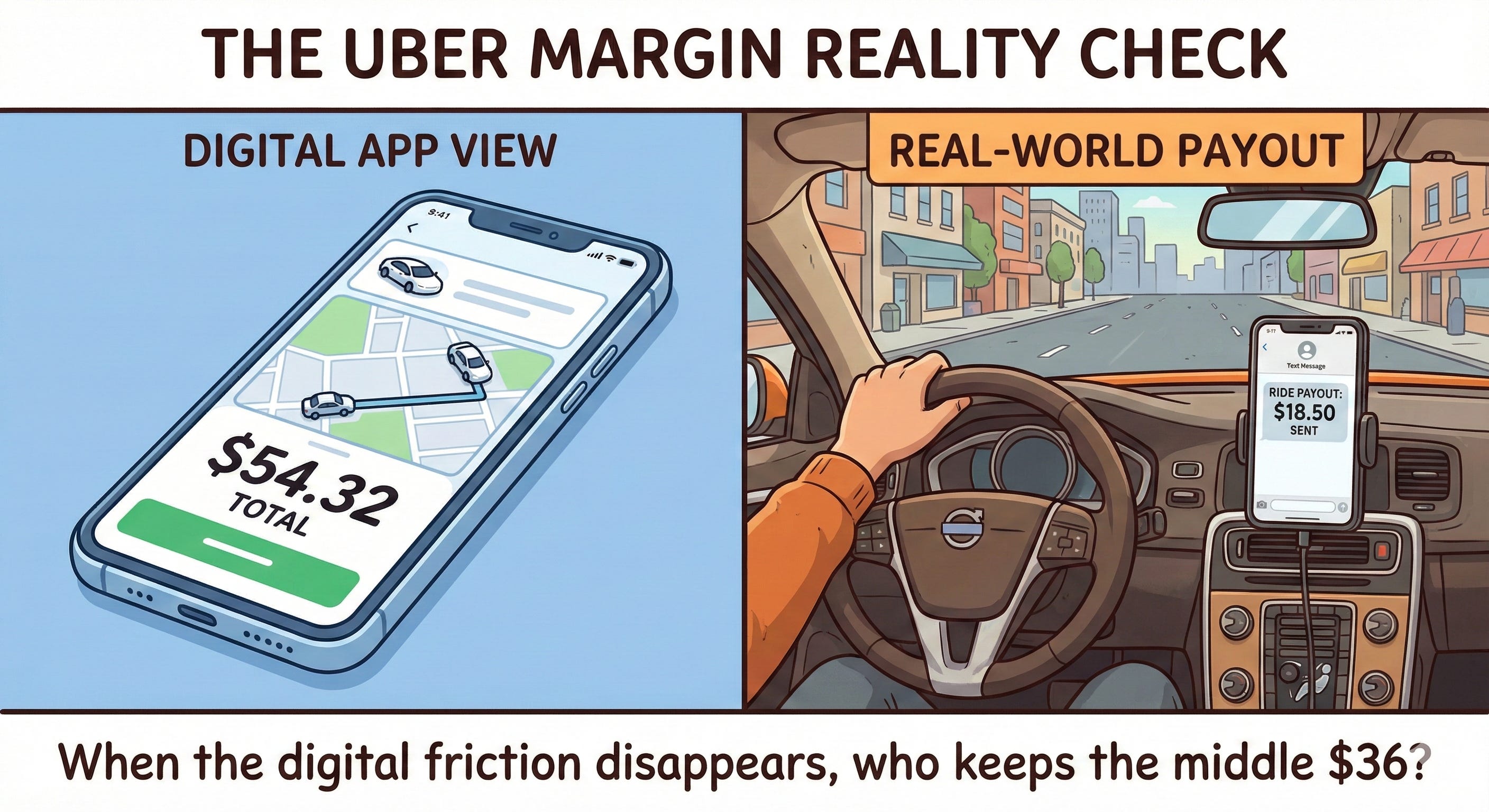

Human-Centric Service Platforms are the likes of DoorDash and Expedia. Initially, upon reading the article, I thought... “Nahhhh.” But pondering the delivery issue for a minute, one could easily see what the article describes playing out.

I took an Uber today that charged me $54 and some change. The driver told me they were getting $18.50 for that ride. I don’t believe the aggregators will be disrupted by 2028, but something does have to give in those margins. Perhaps AI can be the thing to nudge it along.

So then what? Or, The Good

Alright, we’ve got the bad out of the way. I hate that section, I’m an eternal optimist. But under the premise that the 2028 GIC comes true, where would I put my money today?

I’d look to:

“Arms Dealers”

Power & Energy

Vertical moats & specialized manufacturing

Cybersecurity

The “arms dealers” here are the obvious ones. This is the infrastructure behind AI. There are a ton of options: Nvidia, AMD, maybe Intel if you’ve got a wild side. You could look at memory options, data center holders, or perhaps even liquid cooling from Vertiv (VRT) and power management from Eaton (ETN).

The “arms dealers” are an article in themselves. Lots of options, lots of movement. In an effort to help you dig into ideas, look at the holdings of some ETFs covering the sectors:

Data centers: DTCR (Global X Data Center & Digital Infrastructure ETF)

Chips: SMH (VanEck Semiconductor ETF) or SOXX (iShares Semiconductor ETF)

AI Infrastructure: AIQ (Global X Artificial Intelligence & Technology ETF)

Power & energy is right up there too. If more and more knowledge workers are replaced by agents, the bottleneck will be power. Utilities are a play here, as are speculative options in nuclear and small modular reactors (SMRs).

Options on the ETF front to dig into:

The Smart Grid: GRID (First Trust Nasdaq Smart Grid Infrastructure ETF)

The Nuclear/Uranium Play: URA (Global X Uranium ETF)

Broad Utilities: XLU (Utilities Select Sector SPDR Fund)

Vertical moats, those untouchables, they exist. There are disruptors to the likes of Lockheed Martin (Anduril), but companies like LMT will consistently be knocking on the door of government contracts. Other options I’d eyeball here are robotics with names like Teradyne or Intuitive Surgical. Rocket Lab is another interesting name to keep an eye on, and if SpaceX goes public, I’m going all in.

ETFs for idea generation include:

The New Guard: PAIW (WisdomTree Physical AI, Humanoids and Drones ETF)

The Industrial Standard: BOTZ (Global X Robotics & Artificial Intelligence ETF)

Automation Focus: ROBO (Robo Global Robotics and Automation Index ETF)

Finally, Cybersecurity. We’re going to see unimaginable attacks in 2026, I guarantee it. As cool as AI is, it’s currently very susceptible to a variety of attacks that could easily sneak bad packages into your coding pipelines. CrowdStrike is a big name here; Okta, Cloudflare, SentinelOne, and others also have coverage in the space.

ETFs for further research:

The Liquidity Leader: CIBR (First Trust NASDAQ Cybersecurity ETF)

The “Pure Play”: HACK (Amplify Cybersecurity ETF)

W-2 Employee

Investing isn’t the source of most of our income, a steady job is. The article calls for a vicious cycle that wipes out most high-paying knowledge jobs. Those that remain will trend toward lower pay. What can we do to protect ourselves and be ready for such an environment? Simple, make yourself dynamic and anti fragile.

Learn new things, try new experiences. It’s the same advice I think you’d hear at any point, not just when facing AI disruption. But, the specifics?

Well, first and foremost: learn AI. Become a “generalist operator” who has experience orchestrating 10 agents at once. You’ll be worth so much more than a specialist who only knows a single legacy workflow.

Also, consider moving toward the physical world or high-stakes environments and roles.

The physical world can still have tech connections. I’ve always been interested in robotics, so I’m starting to dabble a bit there and building hardware on the weekends. Will I be an all-star robotics engineer by 2028? Probably not. But if the world does suddenly shift, perhaps I’ve got enough exposure to get a job fixing the clankers.

Electronics, woodworking, plumbing, if you’re so inclined. Learning is fun. I’ve always stuck to heavier “hands-on-keyboard” style learning, so branching out can’t hurt.

The one thing I don’t see going away is sales and marketing. I’ve created three apps in the last month, and none of them are exactly flying off the shelves. When code is free, distribution becomes the moat. People with the skills to sell may just be the ones who dominate in the new world.

My Plan

To wrap this up, the 2028 GIC article from Citrini is fiction. Sure, some parts may come true, but it’s more than likely that humans find a way to adapt.

Some of the jobs that exist today, especially at the entry level, will not exist in a few years, and that’s okay. I think we will find ways to help those who are displaced, though there may be bumps along the way.

As I mentioned above, I am taking on new hobbies. I’ll be playing with robots with my young children, and we’ll all be learning new skills along the way.

On the investing front, I am steering clear of software that I believe I could recreate fairly quickly. Sure, there are thousands of edge cases I might miss in building a CRM, but a team of two or three could tackle a niche and make a pretty penny. Rinse and repeat with a hundred teams of two across many niches, and Salesforce is going to have a problem.

Salesforce could overcome those challenges, but they could also struggle for a long time against rising churn. I’m interested in how it plays out, but I won’t have a dog in the fight.

I mentioned at the top that I’m an optimist. And I am. But part of being an optimist is recognizing that growth and prosperity sometimes come through loss. Humans will figure it out, though, we always do.